On this site we are making the Risk-On Risk-Off Index data and documentation publicly available. In exchange for using the data, please give attribution using the following reference: "Risk-On Risk-Off: A Multifaceted Approach to Measuring Global Investor Risk Aversion." We will update the daily and weekly series in real time. We provide below a list of papers to date, to our knowledge, using the index. We would love to hear from you if you use the data. Please send one of us an email at Anusha Chari, Karlye Dilts Stedman, or Christian Lundblad.

Citation: Chari, A., Dilts Stedman, K., & Lundblad, C. (2023). Risk-on risk-off: A multifaceted

approach to measuring global investor risk aversion (Working Paper No. 31907). National

Bureau of Economic Research. doi: 10.3386/w31907.

What is the Risk-On Risk-Off Index? The Risk-on Risk-off (RORO) index is a multifaceted measure designed to capture the realized variation in global investor risk appetite. The measure uses daily data from asset markets in the United States and the Euro area. It presents an aggregation of risk-on risk-off states of the world based on four broad categories reflecting variation in advanced economy credit risk, equity market volatility, funding conditions, and currencies and gold. To infer the overall risk bearing capacity of international investors, the RORO index comprises the first principle component of the daily changes in these series.

The Risk-On Risk-Off (RORO) Data: Daily Series, Weekly Series.

Documentation: Please take a look at this description of how the index is constructed. Read me.

Here is a list of published and working papers using the RORO Index:

Ahmed, R. (2023). Flights-to-safety and macroeconomic adjustment in emerging markets: The role of U.S. monetary policy. Journal of International Money and Finance, 133, 102827. https://doi.org/10.1016/j.jimonfin.2023.102827

Aizenman, J., Cheung, Y.-W., & Qian, X. (2021). International Reserve Management and firm investment in emerging market economies. NBER Working Paper No. 29303. https://doi.org/10.3386/w29303

Chari, A. (2023). Global risk, non-bank financial intermediation, and emerging market vulnerabilities. Annual Review of Economics, 15(1), 549–572. https://doi.org/10.1146/annurev-economics-082222-074901

Chari, A., Dilts-Stedman, K., & Forbes, K. (2022). Spillovers at the extremes: The macroprudential stance and vulnerability to the global financial cycle. Journal of International Economics, 136, 103582. https://doi.org/10.1016/j.jinteco.2022.103582

Chari, A., Stedman, K. D., & Lundblad, C. (2020). Capital flows in risky times: Risk-on/risk-off and emerging market tail risk. NBER Working Paper No. 27927. https://doi.org/10.3386/w27927

Chari, A., Stedman, K. D., & Lundblad, C. (2022). Global fund flows and emerging market tail risk. NBER Working Paper No. 30577. https://doi.org/10.3386/w30577

Eguren-Martin, F., & Sokol, A. (2022). Attention to the tail(s): Global Financial Conditions and exchange rate risks. IMF Economic Review, 70 (3), 487–519. https://doi.org/10.1057/s41308-022-00160-0

Forbes, K., Friedrich, C., & Reinhardt, D. (2023). Stress relief? funding structures and resilience to the covid shock. Journal of Monetary Economics, 137, 47–81. https://doi.org/10.1016/j.jmoneco.2023.05.005

Goldberg, L. S., & Krogstrup, S. (2023). International capital flow pressures and global factors. Journal of International Economics, 103749. https://doi.org/10.1016/j.jinteco.2023.103749

Kalemli-Özcan, Ş., & Ünsal, F. (2023). Global transmission of Fed hikes: The role of policy credibility and balance sheets. Brookings Papers on Economic Activity.

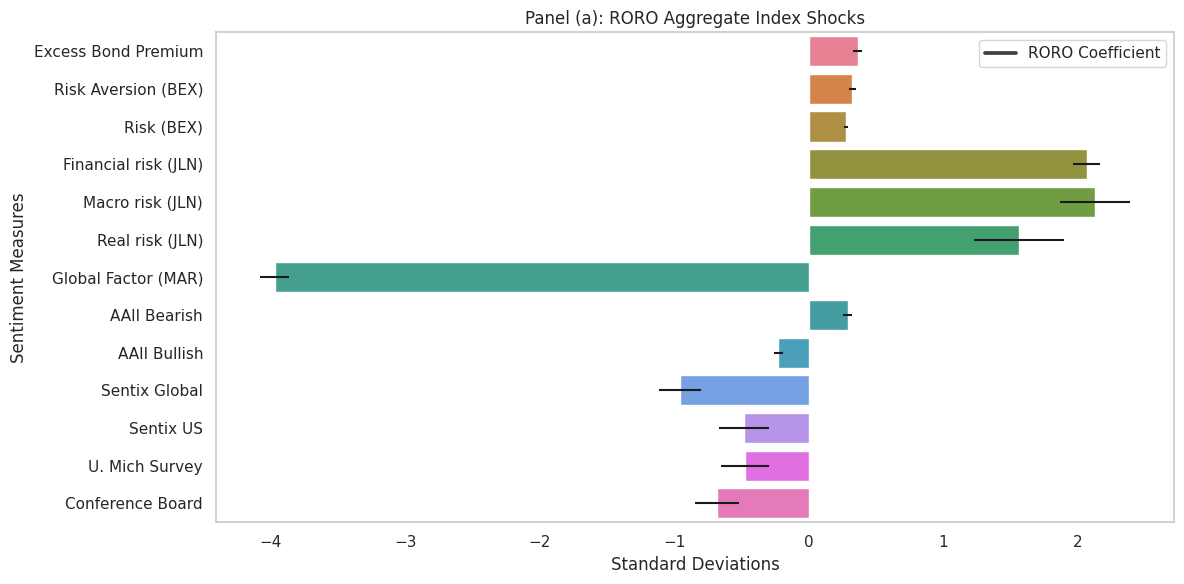

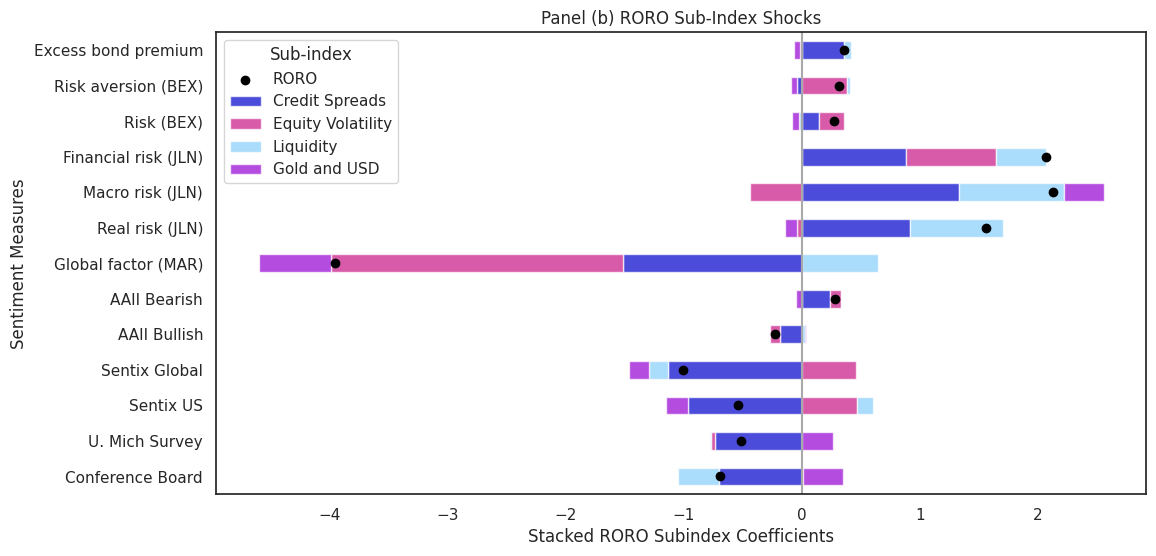

And a figure from our 2023 NBER working paper. Figure 2 (a) shows displays the results regressing alternative measures of sentiment on a one standard deviation shock to the daily aggregate RORO index. Panel (b) shows the loadings of the sentiment measures on subcomponents of the aggregate index.